Brazil is a huge card market. In 2016, Brazilians carried out 5.9 billion transactions with their credit cards, an increase of 6% in comparison to the previous year. Furthermore, last year, over 600 million credit cards were issued in the country as well as nearly twice as many debit cards. However, according to the Brazilian Central Bank, many cards are never activated or used for payment transactions. In fact, just over 50% of the credit cards end up being approved for use and less than one third of the debit cards are activated.

While credit card usage is increasing, it is worth noting that credit cards issued in Brazil are often limited to purchases in BRL. In addition, Brazilian consumers are used to paying in installments when purchasing with credit cards. According to Abecs, BRL 353.1 billion in credit was granted for consumers using installment payments in 2016. This represents 54.4% of the total volume of credit granted to private individuals to finance their consumption of goods and services. However, despite of the popularity of credit cards, a great number of Brazilians are not eligible to own a credit card.

Why do many Brazilians not own credit cards?

There are three main reasons why Brazilians are denied a credit card:

- Unbanked person: Brazil has 55 million unbanked adults and more than 20 million without access to any banking service whatsoever. This limits the penetration of credit cards in the country, as an unbacked person is not eligible to apply for a credit card.

- Name included in Serasa (nome sujo): Serasa is a private Brazilian company, with more than 50 years of history in the country. It is responsible for a complete database containing information on private individuals and legal entities, such as their current debt status. Such information helps issuing banks to determine someone’s eligibility for a credit card. If a person or company has what in Brazil is called “nome sujo” (translated as “dirty name”), meaning they are included in Serasa’s list of debtors, banks won’t approve their credit card request.

- Debt history: Even when consumers don’t have any delayed payment, they can have their request for a credit card denied. This often happens when more than 30% of their income is compromised with the payment of any financing (installments, loans, etc.).

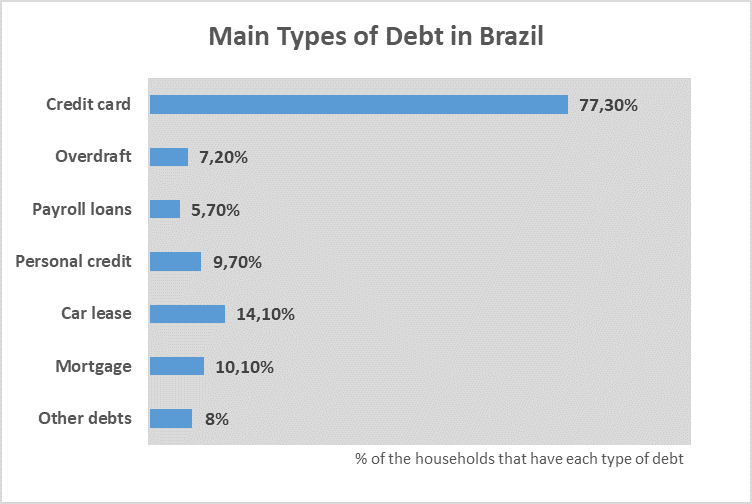

What are the main types of debt in Brazil?

The National Consumer Indebtedness Survey indicated that as of January 2017, 55.6% of the Brazilian households had some type of debt, such as installment purchases with credit cards, car leases, loans or insurance. Furthermore, 22.7% of them have delayed debt and out of those, 9% affirm that they are not able to pay their debts. These are the main types of debt in Brazil, according to the survey:

The difficulties in obtaining a credit card, in addition to the need to reduce their debts, are the main reasons why consumers choose to pay with cash and alternative payment methods, such as boleto bancário. The latter is one of the most democratic payment methods in the country. Brazilians are not required to have a bank account to use it, credit checks are not necessary and last but not least, there is no minimum age to be able to pay with boleto bancário, unlike what happens with credit cards. The local payment method is so widespread that it even transitioned to e-commerce payments and is the second most used payment option in the segment, accounting for nearly one quarter of the transactions.

In light of this, to reach a bigger number of Brazilian consumers, merchants must offer boleto bancário and other alternative payment methods on their online stores. Furthermore, by using a boleto with accelerated payment confirmation, like Boleto Flash®, which is confirmed in under two hours, online businesses can see greater conversion rates. This happens mostly because it allows consumers to carry out impulse purchases, which is often not the case with regular boletos, that can take up to three business days to be confirmed.

Comments

Great article! Thank you for putting time into it. My wife has credit card debt in Brazil. Does it keep compounding at 300% a year????

Hi Elijah. Thank you for your comment. Last month, it was compounding at 271.4% a year, so not a great improvement.

Is there a Bank that is issuing prepaid Visa or Mastercard in Brazil?

Hi David. Yes, Banco do Brasil, for instance, has its Ourocard Pré-Pago which is Visa labeled. Itaú, on the other hand, offers Itaú Pré-Pago with both Visa and MasterCard labels. Regards.

Hi Bianca! Do you know if it’s it possible for a U.S. Citizen to get a credit card in Brasil? I have a CPF number!

Hi Alexa. If you have a CPF and live in Brazil, you should be able to open a bank account and apply for a credit card. However, if you do not live in Brazil, I’m not sure how it would work. Your best option would be to contact local banks to see what your options are.

[…] fact, an estimated 55 million of Brazilian adults are unbanked, while more than 20 million lack access to any banking service […]

My wife and I spend 4-5 months in Brazil (as it is her native country) We are from the USA and have Credit Cards issued there from Banks we use.

In the past 2 years we have found that a lot of places now use a credit card reader that denies International Credit Cards even tho they advertise they take Visa.

Many Taxi’s, Uber, restaurants and even Supermarkets and now using readers that do not accept our cards. It is an embarrassment when you come to pay and possibly do not have the cash. Any suggestions for us? We have always been told it is better to use a credit card instead of cash in another country.

Bill and Tereza Baumgarten

Hi Bill,

Usually, there shouldn’t be any problem with credit card readers, even if you are using an international credit card. However, the cardholder must always make sure that he has authorized operations for international territory before traveling. The best call is to check with your bank if you are all set.

But also, be sure to always carry some cash, as many establishments in Brazil do not take credit cards.

Hello Bianca!

I am a dual citizen US & Brasil thanks to my parents! I live in the USa, but have a CPF and will open a bank account in Brasil. With the current exchange rate so high do you think I can open a credit card in Brasil?

Hi Bianca,

I am trying to open a business in SP. Got a virtual place in a coworking place. Trying to pay them on PagSeguro. Unable due to lack of cell phone and the had to twitch my US address on the application. What is your suggestion. Open an account on a virtual bank, credit card from a local bank, etc? I am BRAZILIAN and do have my CPF.

Hi Bianca, I am a US citizen staying in Brazil with my Brazilian wife. I plan to buy a car. Is there a limit in Brazil on how much a US citizen can spend on their US credit card in Brazil? My Credit limit exceeds the price of a car here in Brazil and my CC company approved of this purchase.

I love

Good article. Quesion: Here in the U.S. you cannot be imprisoned for not paying debt. I have a friend who escaped Vz to go to Brazil. He now owes over $3000 on a Brazilian credit card, which he will probably never be able to pay. The card has been canceled and the debt keeps growing. Can he possibly wind up in prison over this? Like I said, in the U.S. this does not happen, but I have no idea about the laws in Brazil. Thank you.

I just moved to Brazil and need help establishing some credit history so I can be able to purchase a condo or car in the future without paying in cash. Do you know a financial advisor who can help?